LNG market: 4Q 2023

Summary

LNG loadings in the 4th quarter increased to 110.2 million tons. Plus 8.4 million tons compared to the previous quarter and plus 1.9 million tons compared to the 4th quarter of last year. LNG discharges also increased to 108.3 million tons of LNG. The growth is seasonal, due to the cooling in the Northern Hemisphere, where the main energy consumers in general and LNG in particular are concentrated. The impact of El Nino has led to a warm winter in Europe and, as a result, moderate demand for LNG imports to Europe.

The three leading LNG shipping countries are the USA, Australia and Qatar. Australia and Qatar have switched places in the ranking of the leading LNG suppliers.

The top three countries in LNG unloading are China, Japan and South Korea. The positions of importers have not changed compared to the previous quarter.

Mild temperature in Western Europe and Eastern Asia and steady LNG supply were key factors of LNG market in Q4.

One of the key events of the 4th quarter was the increased US pressure on Novatek, its suppliers and customers, in particular, participants in the Arctic LNG-2 project. Earlier, a similar attack was launched on Russian LNG transshipment points in Murmansk and Kamchatka during 2023. In 2022 three lines of the Nord Streams delivering gas from Russia to Germany were blown up. These actions are an integral part of the program to promote American LNG in the markets of Europe and Asia.

Spot LNG prices in the 4th quarter increased relative to the levels of the 3rd quarter and are now in the range of 350-400 dollars per thousand cubic meters. Gas in Europe and East Asia is still expensive, but it is far from skyrocketed level of 3-4 quarters of 2022. High volatility of spot gas prices is traditionally possible in the 1st quarter of 2024. If risk factors are realized, gas prices are likely to rise to $500 per thousand cubic meters and above. In the case of a lack of events in 1st quarter, high gas reserves may lead to a drop in spot prices below the level of $ 300-250 per thousand cubic meters.

Loading

Global LNG discharges in the 4th quarter of 2023, including cabotage and re-export, amounted to 110.2 million tons, which is 8.4 million tons higher than in the previous quarter and 1.9 million tons higher than a year ago.

The USA is the number 1 LNG exporter. Australia and Qatar are also in the top 3 exporters. Russia is ranked 4th. No significant changes compared to the previous quarter.

USA

LNG shipments from the United States in the 4th quarter amounted to 23.3 million tons - plus 1 million tons of LNG compared to the 3rd quarter of 2023 and plus 2.4 million tons of LNG compared to the 4th quarter of 2022. The United States became the largest LNG exporter in the world by the end of 2023 and will remain so for several years.

During Q4 2023 export of US LNG have been mainly headed to Europe, especially in France, United Kingdom, Nederlands, Spain. Main Asian importers of US LNG are Japan, India, South Korea. Customer base of US LNG is the most diversified among all LNG producers.

Also, 442,000 tons of LNG were unloaded at U.S. ports in Q4. A year ago, only one cargo was unloaded.

Details of LNG shipment from the USA are available at the link.

Australia

LNG shipments by Australian LNG plants amounted to 19.8 million tons of LNG in the 4th quarter of 2023. Plus 1.8 million tons of LNG compared to Q3 2023 and minus 1.1 million tons compared to Q4 2022.

The strategic input for the Australian LNG industry is to prioritize the needs of domestic gas demand over LNG exports. The geographical remoteness of gas fields and major cities and industrial centers, taking into account the relatively undeveloped system of internal gas pipelines, is a key obstacle. An additional obstacle is the shareholder structure of Australian LNG projects: major portion of profit from the export of Australian LNG goes outside Australia. Key activities to overcome these obstacles are construction of additional local gas pipelines (for example, the expansion of the South West Queensland pipeline, the expansion of the Moomba-Sydney gas pipeline), as well as construction of regasification terminals in southeastern Australia, and the expansion of gas production at the Otway field.

Details of Australia's exports are available at the link.

Qatar

LNG shipments by state-owned QatarEnergy LNG from its two plants Qatargas (the largest in the world) and RasGas in Q4 amounted to 18.5 million tons of LNG - minus 1.6 million tons of LNG compared to Q3 2023 and minus 1.7 million tons of LNG compared to Q4 last year.

Qatar's main efforts are focused on the construction and contracting of future supplies of the expansion of the QatarGas plant with a total capacity of 49 million tons of LNG. The launch of 6 trains will be carried out sequentially in 2025-2027. This construction is so large that only new additional capacities would take the honorable 4th place in the ranking of exporting countries.

Details of Qatar's exports are available at the link.

Russia

LNG shipments in the 4th quarter of 2023 increased to a record 8.7 million tons of LNG per quarter. Plus 2.0 million tons to the volume of the 3rd quarter of 2023 and plus 0.2 to the volume of the 4th quarter of 2022. LNG is loaded at Sabetta (Yamal LNG plant with an annual capacity of 17.4 million tons of LNG) and Prigorodnoye (Sakhalin-2 plant with an annual capacity of 9.6 million tons), as well as at Portovaya (Gazprom LNG plant with capacity of 1.5 million tons) and Vysotsk (Cryogaz-Vysotsk plant with an annual capacity of 660 thousand tons). Russia ranks 6th in terms of LNG plant capacity, but is ahead of Malaysia and Indonesia in terms of actual LNG production, which allowed it to take 4th place in the ranking of exporters in the 4th quarter of 2023.

In mid-December, the first train of the next Russian megaproject in the LNG industry, Arctic LNG-2, was launched. The plant with a total capacity of 19 million tons of LNG per year (after the launch of all lines) is destined to go through a series of American obstacles from the very first day of its operation. American pressure is directed at the following key aspects of LNG exports from the Arctic LNG-2 projects, as well as Yamal LNG":

Sanctions pressure on traders from controlled and neutral countries buying Russian LNG. The pressure is primarily in terms of the introduction of secondary sanctions for such trading companies, which is vital for them. It is worth expecting exceptions from sanctions on some supplies for Japanese, Chinese and Indian companies, as was the case with supplies from the Sakhalin-2 project.

Sanctions pressure on shipyards and shipping companies that own a fleet of gas carriers. This has already led to massive cancellations of the construction of ice-class gas carriers necessary for the export of LNG from Arctic projects. It is the availability of a sufficient fleet and restrictions on the spot freight of third-party gas carriers that is the key sore point of Russian LNG exports. There are no quick solutions by analogy with a sharp increase in our own oil fleet. There is a shortage of LNG gas carriers in the world, most of the gas carriers are controlled by LNG producers or European and American oil and gas companies. The creation of domestic gas carriers is in full swing, but technology testing and the construction of a large-scale fleet will take a decade.

Sanctions pressure on equipment suppliers, primarily with American and European residence permits. Technological schemes for new projects will obviously be changed, which will shift the implementation of all subsequent projects to the right. For existing projects, we will have to look for alternative options for technological maintenance and repairs. It will be more expensive and longer, but it is feasible and will allow increasing technological expertise within the country.

The complex of measures taken in the country will not only overcome this pressure, but also create the foundation for Russia's entry into the top three LNG exporters. However, this will affect export volumes only in the 2030s, but for now it remains to hope for multilateral compromises that will allow LNG exports to continue at least in current volumes.

Details of shipments of Russian LNG are available at the link.

Malaysia

Shipments of Malaysian LNG in the 4th quarter amounted to 7.0 million tons of LNG. A quarter earlier, there were 676 thousand tons of LNG less. A year ago, it was 352 thousand tons more LNG. The main Malaysian LNG producer is the Bintulu MLNG plant.

Malaysia also unloaded 834 thousand tons of LNG in the quarter under review to meet domestic demand. Which is slightly less than the indicator of the 4th quarter of 2022 - 946 thousand tons.

PFLNG Satu

Details of Malaysia's exports are available at the link.

Indonesia

Indonesia shipped 3.7 million tons of LNG in the 4th quarter of 2023. Plus 0.5 million tons compared to the indicator of the 3rd quarter. Minus 0.7 million tons compared to the indicator of the 4th quarter of 2022.

Donggi-Senoro LNG

During the quarter under review, Indonesia unloaded 215 thousand tons of LNG in its own ports to meet domestic demand.

Algeria

Algeria, a pioneer in the LNG industry, exported 3.6 million tons of LNG from its two LNG plants Arzew and Skikda in the 4th quarter of 2023. Plus 264 thousand tons compared to the volume of the 3rd quarter. Plus 479 thousand tons compared to the indicator of the 4th quarter of 2023.

The main exports of Algerian natural gas are still carried out through pipelines to Spain and Italy.

LNG and Algeria's export gas pipelines

Details of Algerian exports are available at the link.

Nigeria

Nigeria exported 3.1 million tons of LNG in the 4th quarter of 2023. This is two cargos higher than in the previous quarter, but one less cargo than a year ago.

Nigerian LNG Plant

Oman

Oman exported 3.0 million tons from the country's only LNG plant, Qalhat, which is at the level of the previous quarter.

Qalhat LNG Plant

Trinidad and Tobago

LNG exports from the country's only LNG plant Atlantic LNG, owned mostly by European oil and gas companies, amounted to 2.1 million tons in Q4, which is 337 thousand tons more than in Q3, which saw a similar drop in output volumes. LNG output continues to remain significantly below the combined nominal capacity of the plant's 4 lines, amounting to 4 million tons per quarter.

Atlantic LNG Plant

Papua New Guinea

Papua New Guinea's LNG exports from its only LNG plant continue to be steady and amounted to 2.0 million tons of LNG in the quarter under review, which is close to 100% of the plant's nominal capacity.

Papua LNG

UAE

Exports from the UAE's only LNG plant ADGAS on Das Island in the 4th quarter amounted to 1.4 million tons.

ADNOC LNG Plant

205 thousand tons of LNG were unloaded in the UAE ports in the 4th quarter, half the figure of the previous quarter.

Brunei

Exports from the Brunei LNG plant in Lumut amounted to 1.3 million tons in the 4th quarter. Brunei LNG Sendirian Derhard is owned by the Government of Brunei (50%), the American Shell Overseas Trading (25%) and the Japanese Mitsubishi Corporation (25%).

Brunei LNG Plant

Norway

Exports of Norway's only LNG plant Hammerfest LNG Snohvit amounted to 1.1 million tons in Q4, rising from 1.0 million tons a quarter earlier. The main gas exports from Norway are carried out through pipelines and exceed LNG exports by two orders of magnitude.

Hammerfest LNG Snohvit

200 thousand tons of LNG were unloaded in Norwegian ports, at the same level as in previous quarters.

It is worth noting that the volume of LNG re-exports in the ports of Singapore and Belgium exceeded 1 million tons of LNG per quarter. This indicates a growing volume of speculative physical LNG trading.

All other countries exported less than 1 million tons of LNG in the 4th quarter of 2023. Detailed export statistics by country are available at the link.

Discharge

Global LNG discharge in the 4th quarter of 2023 amounted to 108.3 million tons, which is 9.2 million tons more than in the previous quarter. This indicator takes into account the import of re-exported LNG and cabotage shipments, but does not take into account the accumulation of LNG “on the water".

East Asian countries - China, Japan and South Korea - continue to top the ranking of LNG importers.

China

LNG offloads in China in the 4th quarter amounted to 18.5 million tons of LNG. This is 2.2 million tons of LNG more than in the 3rd quarter and 0.4 million tons less than in the 4th quarter of 2022.

LNG re-export in the 4th quarter amounted to 387 thousand tons. China is trying to monetize existing long-term contracts for the supply of LNG at oil prices and pipeline gas supplies.

Japan

LNG offloads in Japan in the 4th quarter of 2023 amounted to 16.9 million tons of LNG, which is 0.8 million tons more than in the 3rd quarter. Offloads in the 4th quarter of last year were higher - 17.5 million tons of LNG.

The re-export of LNG by Japan in the 4th quarter amounted to 87 thousand tons.

South Korea

12.3 million tons of LNG were unloaded in the ports of South Korea. Plus 2.7 million tons compared to the indicator of the 3rd quarter. Minus 654 thousand tons compared to the indicator in the 4th quarter of 2022.

The re-export of LNG by South Korea in the 4th quarter amounted to 316 thousand tons.

India

India imported 6.3 million tons of LNG in the 4th quarter of 2023 and became the number 4 importer in the world.

The largest consumers of natural gas in India are fertilizer production, electric power and urban consumers. Fertilizer producers are guided by operating margins - a decrease in the price of fertilizers and an increase in the price of LNG reduces the volume of purchases. The Indian energy sector is dominated by coal, where Coal of India reigns supreme. However, the desire to improve the local environment, operational problems with the operation of coal-fired thermal power plants and the supply of coal, and the growing population encourage the government to develop gas generation and LNG imports. Currently, India has about 25 GW of installed gas generation capacity with peak demand of the entire electricity market of 243 GWh/h. That is, gas-fired thermal power plants cover up to 10% of peak electricity demand. However, LNG consumption by the electric power industry is highly sensitive to the import price. The Government of India is actively investing in the construction of urban gas networks and gas filling stations. All this stimulates a long-term growth in demand for LNG imports.

India may become one of the largest buyers of Russian LNG by analogy with the redirection of Russian oil flows from Europe to India. The Indian government prioritizes the needs of a growing domestic market over the need to please Washington. However, they try to avoid direct risks of secondary sanctions on formal grounds. However, there remains the question of the possibility of physical delivery of LNG from the Arctic to India. Currently, Qatar is the key LNG supplier to India. Other major suppliers are the USA, UAE, Algeria, Angola, Trinidad and Tobago, Oman. Given the geography and difficulties of crossing the Panama Canal, it will be possible to compete for the share of the United States and Trinidad and Tobago.

France

France was the largest LNG importing country in Europe at the end of the 4th quarter with an indicator of 6.1. Plus 1.6 million tons of LNG compared to the indicator of the 3rd quarter. Minus 1.7 compared to the indicator of the 4th quarter of last year.

France has further increased its import capacity - the Cape Ann floating storage facility has arrived in Le Havre in the north of the country.

The re-export of LNG by France in the 4th quarter amounted to 352 thousand tons.

Details of LNG imports by EU countries are available at the link.

Taiwan (Province of China)

Taiwan imported 5.2 million tons of LNG in Q4. LNG imports to Taiwan are stable and do not change much from quarter to quarter.

Spain

Spain imported 4.3 million tons in the 4th quarter of 2023, which is at the level of the previous quarter. A year ago, imports were 1.2 million tons higher. Spain is the number 2 LNG importer in Europe.

The re-export of LNG by Spain in the 3rd quarter amounted to 512 thousand tons.

Details of LNG imports by EU countries are available at the link.

Netherlands

The Netherlands imported 4.1 million tons of LNG in the 4th quarter, which is at the level of the 3rd quarter. In the 4th quarter of last year, imports were 473 thousand tons less.

LNG re-exports amounted to 170 thousand tons of LNG in the quarter under review.

Details of LNG imports by EU countries are available at the link.

Singapore

Singapore imported 3.6 million tons in Q3, which is significantly more than in Q3 - by 1.2 million tons of LNG. This volume of LNG unloading and transshipment is a record for Singapore during the entire observation period.

Singapore's LNG re-export in the 4th quarter amounted to 1.2 million tons of LNG. Singapore is a leading energy hub for transshipment of oil, petroleum products and LNG.

Details of the import and re-export of LNG by Singapore are available at the link.

United Kingdom

The UK reduced the volume of LNG imports from 4.9 million tons of LNG in Q2 to 0.9 million tons in Q3, which is natural for it - low summer demand is covered by its own production, and low UGS capacities do not allow storing gas for the winter. In the 4th quarter, the UK imported 3 million tons of LNG, which is half the figures for the winter quarters of last year.

Details of LNG imports by UK are available at the link.

Belgium

Belgium imported 3.1 million tons of LNG in the 4th quarter of 2023, which is more than in the 3rd quarter - 2.3 million tons. The temporary decrease in imports in the 3rd quarter and early 4th is due to 100% occupancy of European UGS by the time the gas winter begins.

The re-export of LNG by Belgium in the 4th quarter amounted to 1,033 thousand tons of LNG. Therefore, the demand for LNG imports is primarily characterized by price dynamics and arbitrage, rather than the demand of the local market itself.

Details of LNG imports by EU countries are available at the link.

Türkiye

Turkey imported 2.4 million tons of LNG in the 4th quarter of 2023. The sharp increase after the summer quarters is due to seasonal demand for gas for heating.

Italy

Italy imported 2.0 million tons of LNG in the third quarter, which is 1.0 million tons less than in the second quarter. The temporary decrease in consumption in the 3rd quarter and the beginning of the 4th is similar to the dynamics of consumption in other European countries.

LNG re-export in the 4th quarter amounted to 245 thousand tons.

Details of LNG imports by EU countries are available at the link.

Egypt

Egypt imported 2.0 million tons of LNG in Q4. 0.9 million tons more compared to the 3rd quarter. The key reasons are the decrease in the flow of pipeline gas from Israel against the background of their war with Palestine, as well as the growing domestic demand for energy. Egypt's population is growing rapidly (1.7% per year) and currently stands at 107 million people.

At the same time, Egypt's LNG exports amounted to 789 thousand tons in the 4th quarter in total for its two LNG plants Damietta and Idku. Thus, Egypt turned from an exporter to a net importer in Q3.

Pakistan

This populous Asian country (224 million people) imported 1.8 million tons of LNG, which corresponds to the average level of imports in previous quarters. Per capita energy consumption is lagging behind at a very low level and has a high potential for growth. But the poverty of the population and high risks for infrastructure projects hinder the growth of LNG imports.

By analogy with oil, Pakistan may become one of the new consumers of Russian LNG. However, the Pakistani authorities will demand a substantial discount compared to market quotations.

Thailand

The volume of LNG imports by Thailand in the 4th quarter amounted to 1.7 million tons of LNG. 0.7 million tons less than in the 3rd quarter of 2023 and 0.6 million tons more than in the 4th quarter of 2022.

It is worth noting the statements of the Ambassador of Thailand to Russia about Thailand's strategic interest in Russian LNG. Perhaps these and other new clients for the Arctic LNG-2 portfolio will help to realize the gas of this project. However, of course, for a good discount to international quotes.

Kuwait

Kuwait imported 1.3 million tons of LNG in Q4. Which is 1.5 million tons less than in the 3rd quarter. It is the 3rd quarter that is the peak in terms of electricity demand in the Middle East - traditionally July and August are the hottest months and, accordingly, require the highest energy consumption for air conditioning. The temperature in the 1st and 4th quarters is comfortable and requires minimal air cooling. Kuwait is the largest importer of LNG among all countries in the Middle East.

Poland

Poland imported 1.2 million tons of LNG in Q4 through its only Svinoujscie regasification terminal, which is at the level of previous quarters. Poland's energy sector remains predominantly coal-fired, with natural gas used for heating, shunting gas generation and as raw materials for chemical companies.

All other countries imported less than 1 million tons of LNG in the 4th quarter of 2023. Detailed import statistics by country are available at the link.

Price dynamics

Asia

Average crude oil quotes are the basis for formulas for long-term LNG supply contracts. Crude oil prices in terms of energy units of gas are usually a resistance level for the spot gas market. When gas reaches this level, some buyers may switch to burning oil instead of gas, reducing demand. In Asia, three quarters of LNG supplies are carried out under long-term contracts and depend on oil prices. Additionally, price fluctuations are smoothed out by averaging the prices of all gas resources imported by China. Thus, East Asian countries are the least sensitive to price fluctuations in the spot gas market.

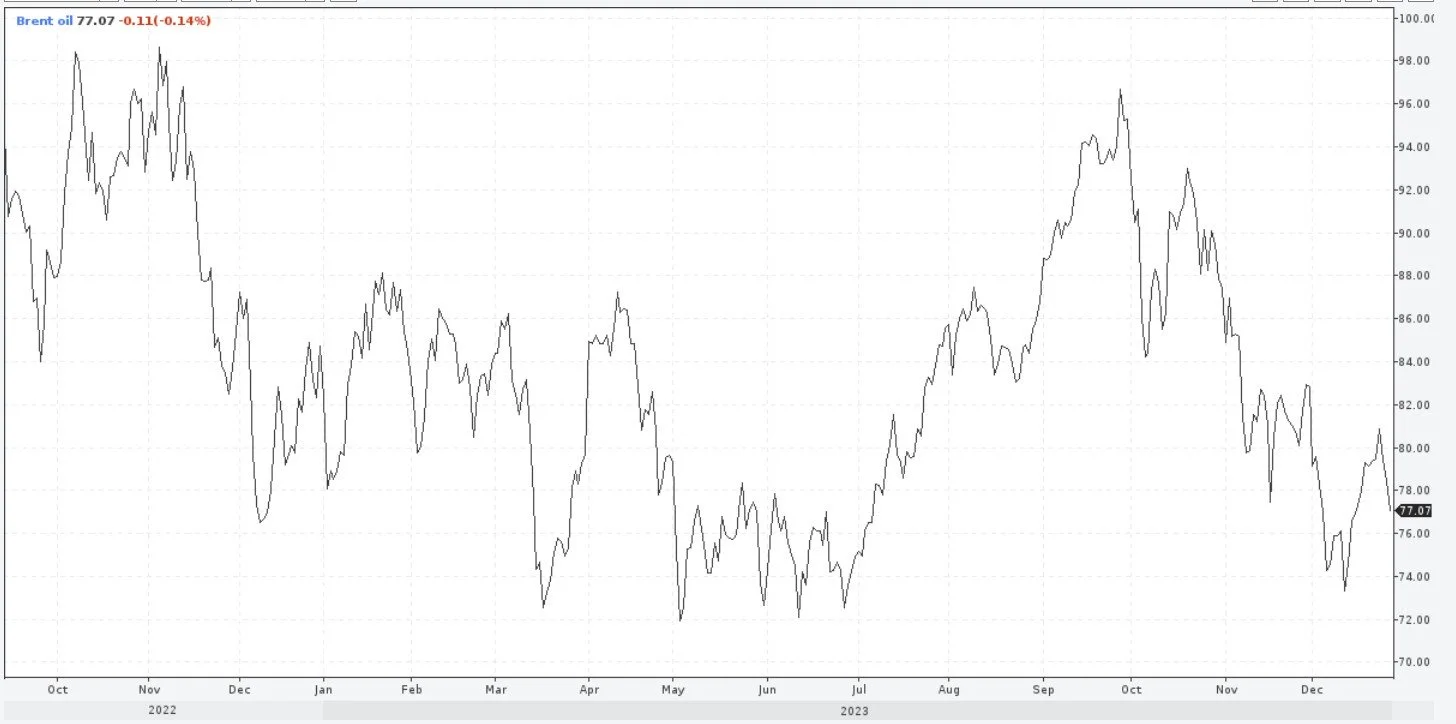

Brent last 12 months

EU

Gas prices in the 4th quarter of 2023 turned from an annual downward trend and began to grow seasonally in October. Due to the fact of warm weather in Europe and East Asia in the 4th quarter and, as a result, high volumes of natural gas reserves in UGS, exchange prices for gas adjusted downward in November and December. The current spot price for gas in Europe on January 1, 2024 is $366 per thousand cubic meters.

Exchange prices for gas at the TTF hub (Netherlands) in the last 12 months, dollars per thousand cubic meters

Despite the significant decrease in gas prices after the energy crisis in Asia in 2021 and Europe in 2022, they are still above long-term averages. Gas in Europe and in the world, on average, is still very expensive.

Exchange prices for gas at the TTF hub (Netherlands) in 2010-2023, dollars per thousand cubic meters

Russia

Domestic gas prices in Russia are still among the lowest in the world, but have no impact on LNG exports from Russia - the systems of gas production, production and export of LNG by Yamal LNG and Sakhalin Energy plants are technologically independent of Gazprom's Unified Pipeline Network. Only the medium-tonnage plants of Novatek Cryogaz-Vysotsk and Gazprom Portovaya consume mains gas.

USA

American gas prices (Henry Hub) remained low during the 4th quarter, which still keeps the margin of LNG supplies from the United States to Europe at a high level.

A brief forecast of the LNG market in the 4th quarter of 2023 - the 1st quarter of 2024 (gas winter)

The first half of the gas winter of 2023-2024 passed quietly. Winters in Europe and East Asia are warm, which leads to planned gas consumption and sufficient reserves of natural gas in UGS.

Key factors that may lead to an increase in gas prices relative to current futures levels:

Low temperatures relative to the long-term norm in East Asia and Europe are key importers of LNG.

Possible attacks and new political restrictions on the remaining Russian pipeline exports to Europe (transit through Ukraine) and Turkey (Blue and South Stream) and, accordingly, the growing demand for LNG imports from Europe and Turkey. Russian pipeline gas supplies are no longer systemically important for the European gas market, as they were a couple of years ago, but their further decline may disrupt the fragile balance of the European gas market.

Possible future political restrictions by Western countries on Russian LNG supplies, primarily to Europe.

The continuation of the drought in the Panama Canal. According to the practice of recent years, it is in the 1st quarter that the longest queues for crossing the Panama Canal are observed. For example, as of January 1, 2024, the queue to enter the channel is about 40 days. This factor affects the supply of all American LNG to Asia.

The intensification of the Israeli-Palestinian war and the involvement of other Middle Eastern countries in the conflict will reduce the availability of the Suez Canal.

Breakdowns and weather restrictions at U.S. LNG plants.

Strikes at Australian LNG plants.

Key factors that may lead to lower gas prices relative to current futures levels:

Warm winters in East Asia and Europe.

The active growth of Russian gas supplies to Central Asia and transit through it to China and, as a result, a decrease in China's demand for LNG imports.

A potential conflict between mainland and island China could trigger a sharp decline in LNG supplies to mainland and especially island China.

Notes:

Advanced real-time analytics for LNG trade are available by subscription (please contact us via info@seala.ai).

Join Seala AI Linkedin page to be informed for all new future releases with new dashboards and insights.